OfficeLindsay SaundersWed 20 May 26

Rent Mismatch Constricts National Office Pipeline

Australia’s office development pipeline is expected to shrink further as soaring construction costs and tighter financing conditions push the feasibility of new projects increasingly out of reach.

According to a new report from Cushman & Wakefield, The Cost to Build: Rising Economic Rents are Constraining New Office Supply, construction costs are forecast to continue climbing through to 2028 across all major CBD markets.

Brisbane is tipped to record the steepest increases.

The research points to a growing disconnect between current market rents and the “economic rents” required to justify new office developments, leaving much of the national pipeline stalled despite improving conditions in some markets.

Cushman & Wakefield associate director of national research Jake McKinnon said rents across Australia remained below the levels needed to support most new office projects.

“Even in the strongest market, rents are not high enough to support most new office projects across Australia,” McKinnon said.

“While rental growth will narrow the gap over time, most markets are likely to see limited new supply until vacancy tightens and occupier demand lifts more uniformly.”

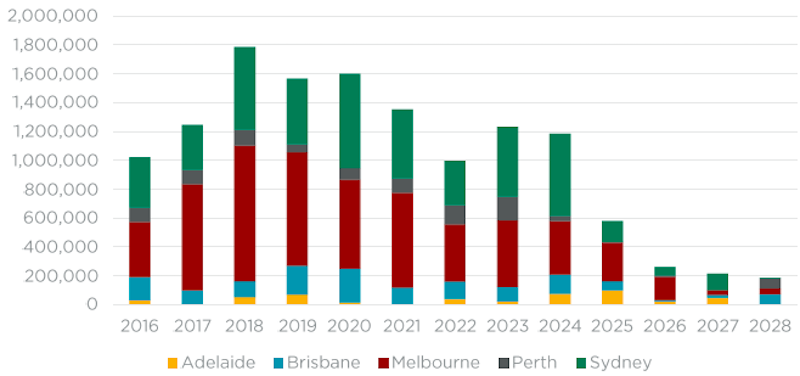

National office supply pipeline in square metres

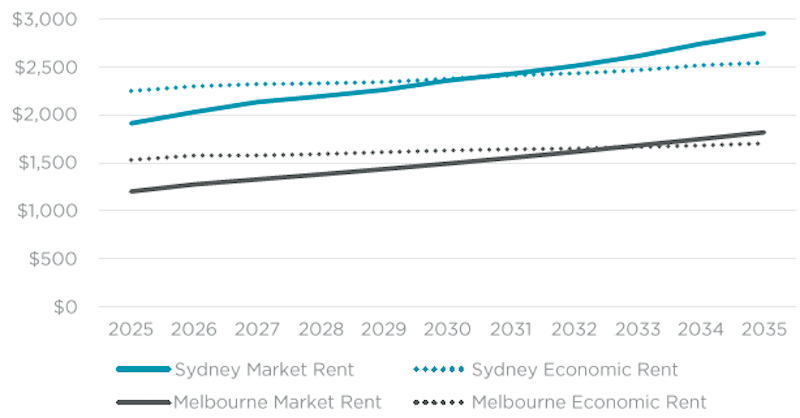

The report found Sydney was closest to viability, with market rents sitting about 18 per cent below economic rents, followed by Melbourne at 27 per cent, Brisbane at 28 per cent, Adelaide at 36 per cent and Perth at 39 per cent.

Sydney and Melbourne are expected to lead the next phase of office development recovery, with both markets showing a clearer path towards narrowing the gap between market and economic rents over time.

By contrast, Brisbane, Adelaide and Perth are not expected to experience the same recovery trajectory under current market conditions.

McKinnon said elevated construction costs were only one part of the challenge facing the sector, with tighter lending conditions and higher pre-commitment hurdles also weighing on new supply.

“Tighter lending conditions, more conservative risk pricing and stronger pre-commitment requirements are also restricting new supply, leading to some projects being delayed, deferred or reworked,” he said.

Cushman & Wakefield head of project development services Hutch Bykerk said constrained supply would increasingly affect occupiers and landlords.

Market v economic rent

“For occupiers, competition for modern, high-quality office space is likely to intensify as the development pipeline remains limited, placing upward pressure on occupancy costs for premium assets over time,” he said.

Bykerk said the environment was also increasing the appeal of refurbishment and repositioning strategies for existing buildings.

“Repositioning existing assets can deliver compliance upgrades, quality, amenity and sustainability outcomes faster while attracting potential tenants at a lower cost compared to a ground-up development,” he said.

The report said adaptive reuse, targeted reinvestment and asset repositioning were likely to remain the preferred strategies for investors and landlords while ground-up office developments remained highly selective.